Fixed Deposits – at best a way to preserve your wealth

India is a growing economy & has moderate-high inflation. The reason FDs are at 8% is that the Govt itself can only borrow in the world at 7%. FDs return 8%, so about 6% at best after tax. With Inflation somewhere in the 5-6% range, the real return on FDs is close to 0; inflation eats away all those returns. A 5-year FD demonstrates this : Invest 1L for 5y at 8% per year. You get 8K pre-tax for 5 years, and then your 1L back after 5 years.

You’ve enjoyed 8K per year which you’ve either spent or re-invested, but at the end of 5 long years, you get precisely 1L (your principal back).

If inflation is 5% per year, your 1L five years from now will be worth 78K in actual spending power. (1L/1.05^5)) i.e you lose money & the hope is that the interest you’ve been paid over the 5-years somehow makes up for the loss. Net net, you would not have grown your wealth, only preserved it.

FDs are thus a decent way (at best) to preserve your wealth. Anyone who keeps their savings in FDs is guaranteed to not be growing their wealth. Banks, however would Love for you to keep your money with them perpetually.

How much of one’s Net Worth should one allocate to FDs? I’d say keep enough for a rainy day, for hospital / emergency needs and think of shorter term deposits – continuously renewing 3 month FDs are a good option.

Gold

Another way to preserve your purchasing power over time is to buy gold. The rupee is a “fiat currency”, like every other currency in the world. It is guaranteed to depreciate every year, making your savings worth lesser over time. You could preserve your wealth via FDs, but if that is the intent, you may be better off preserving it via an investment in Gold instead. Exchanging your paper currency and savings for this precious metal is a 5000-year old way to preserve your purchasing power. It is universally accepted as real money and stands the test of centuries.

In contrast to FDs, which helps the banking system, Gold is “outside” of it. It contributes Zero to the economy, and its Value Add is 0, it is a perfectly “unproductive” asset.

Indians (& Chinese) happen to be among the biggest gold hoarders on our planet. Our societies, to their detriment – disproportionately value gold as a measure of wealth, status and power. India in particular hoards at a tremendous rate every year around festivities & weddings. Having repeated this behavior over the millennia, Indians have accumulated gargantuan amounts of physical gold (see this & this), estimates run somewhere between 25-35 thousand tons. Given these holdings are “off the radar” and very hard to track, the Indian government is trying hard to encourage Indians to get Out of gold and turn, even if slightly, towards productive uses of this wealth. India badly needs its citizens to invest in the future of the country – its enterprises. Those who Are earning, and creating wealth deploy it sub-optimally in Gold and FDs, when it could, for example, be used to finance new irrigation systems & new industries.

Gold should simply be used at most as a wealth preservation tool, it helps preserve purchasing power over long periods of time. Rupees 1 Lac can buy you a basket of goods and services today, but 10 years later, the same paper money of 1 Lac if you kept it under the mattress, will only buy you 61 thousand rupees worth of goods and services (at 5% inflation). If you chose to keep the 1 Lac today in physical Gold, you can expect to have roughly the same purchasing power 10 years down if you convert that Gold back to INR.

Gold is thus Not a way to create & compound wealth.

Real Estate

Real estate is generally not an avenue to build long term wealth; none of the world’s wealthiest individuals / families are hoarders of land or property. But the lure for it is almost always present, because others are often talking about it, so it is “in the air”. More, one typically hears only of prices going up, so it appears that it is a perpetually appreciating asset. These, and other psychological factors keep up an extreme unhealthy to make money out of RE.

Real Estate is not “meant” to make money. People “flip” real estate just as they “flip” companies, buy & sell like traders within some time period to “make nice money”. First, trading – in anything does not add any value to the economy, and can be thought of as “unproductive”. Having said that, the past experience (2001-‘13) of such trading / flipping of Real estate in India, has been often quite positive and profitable. Most involved have done very well for themselves.

What’s often missing when people talk glowingly about how much they bought and sold RE for is a) opportunity costs b) taxation. An example would help :

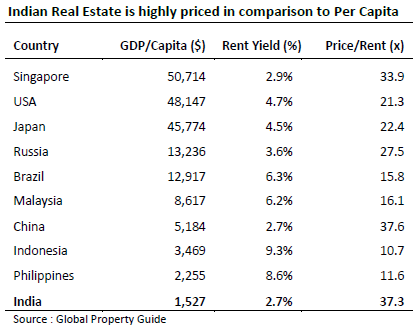

Consider a flat bought in late 2003 for 25L & sold for 2013 for 1.25 crores. Sounds like a fantastic investment which made 1 crore profit & a 17.5% CAGR over 10 years. If you get the sale price in a cheque, the actual money you receive after adjusting for the Govt’s cost inflation index & capital gains taxation is more like 103L, which is only a 15% CAGR. Run-of-the-mill mutual funds did better than 15% over the same 10-year period. But there’s another challenge. How do you invest the reeived monies? If you minimize tax & take large monies in cash, the govt will allow you to avoid capital gains if you invest the proceeds in tax-free bonds (very low return investment) OR in Real estate. Consider the prices of Real Estate (charts below) – at these high entry levels, you are guaranteed a rather low rate of return.

By mid-2016, buying RE in India had become almost unaffordable. Residential real estate pricing in metros had reached stratospheric levels (see Manish Bhandari’s piece on this), grossly out of line with affordability. Please consider the following

See Price / Rent ratio of India in context of its GDP / capita

And this :

Note the bizarre divergence between commercial & residential prices. Remember too that in general commercial real estate tends to receive much higher rents than residential property, magnifying the insanity.

Buying a house to live in is different from investing in RE as an asset. However, here too the Price you pay is crucial, and cannot be at a level which leaves you without sufficient “savings excess” every month that helps to build long-term wealth. Living below one’s means is key. Here’s an excellent article by Yamini Sood on the emotional aspect of having a dweling of your own.

Further Reading :

See legendary investor Li Lu’s talk “The Prospects for Value Investing” (from Oct 2015), pages 5 -13, where he addresses the question :

“from a long-term perspective, which financial assets can grow in a sustainable, effective, safe and dependable manner?”

[Lu has the rare distinction of being considered by Buffett & Munger as a potential successor to manage Berkshire’s investment portfolio. Munger (even as of Feb 2017) has only 3 primary investments – Berkshire, Costco, and an investment in Lu’s fund, Himalaya Capital]